Financial markets process information at a scale that constantly tests the physical limits of modern computing hardware. Every single second introduces thousands of new pricing points, geopolitical developments, and shifting economic data sets. Professional asset managers and retail traders alike rely on rapid data ingestion to maintain a logical advantage in a chaotic environment. Classical computers struggle under the immense weight of these compounding variables because their underlying architecture has physical boundaries. The hardware eventually limits how fast a system can analyze global market conditions. Understanding the transition from human analysis to algorithmic execution requires a look at the actual physics of data processing.

Standard retail trading tools often lag behind the actual reality of the market. Information asymmetry defines who holds the advantage in financial transactions. The organizations and individuals with the fastest analytical engines process the news before the rest of the market can react. Mathematical models have steadily replaced intuition on the trading floor. This transition necessitates an understanding of computational mechanics, statistical probability, and secure operational practices. This guide breaks down exactly how mathematical automation changes the modern approach to asset management.

The Processing Bottleneck in Traditional Finance

Binary computing operates on a strictly linear methodology. A standard processor reads every data state as either a zero or a one and solves mathematical problems sequentially. If an analyst needs to assess the relationship between one hundred different stock prices during a sudden volatility spike, a classical computer must calculate each possible correlation one after another. This sequential processing creates a distinct physical bottleneck. Financial markets do not operate sequentially. Supply chain disruptions happen concurrently with currency fluctuations, regulatory announcements, and consumer demand shifts.

When an institutional trading desk runs risk models on thousands of open equity positions, standard binary hardware requires hours to generate a reliable set of outputs. By the time the risk assessment finishes processing, the market has already moved to a different baseline. High-frequency trading firms spend billions of dollars attempting to shave microseconds off data transmission times. They lay straight-line fiber-optic cables through mountain ranges to achieve a fractional speed advantage over their competitors. They physically place their servers adjacent to the exchange matching engines.

Despite all these physical infrastructure upgrades, the underlying calculating engine itself remains bound by the strict constraints of the Von Neumann architecture. A central processing unit can only execute so many instructions per millisecond. Adding more server racks eventually yields diminishing returns due to the heat generated and the electricity required to power massive data centers. The finance sector hit a hard ceiling on what classical processors could achieve with rapidly expanding datasets.

How Machine Learning Changed the Baseline

Machine learning temporarily bypassed some of the hardware limitations by changing how computers analyzed data streams. Instead of relying on hard-coded trading rules, engineers developed neural networks designed for deep pattern recognition. These networks ingest decades of historical pricing charts to identify recurring sequences that humans miss entirely. A highly trained algorithm might notice that a specific industrial stock historically drops exactly two percent whenever global shipping volumes decline over a specific weekend period.

This predictive capability allowed quantitative funds to automate their equity execution based strictly on mathematical probability. Standard artificial intelligence works exceptionally well when the underlying market rules remain stable. It relies heavily on probability distributions derived completely from past events. Neural networks require massive amounts of structured data to draw accurate conclusions about the future.

A sudden macroeconomic shock breaks these retrospective models. When variables multiply exponentially during an unprecedented market crisis, classical machine learning systems struggle to calculate the new probabilities quickly enough. The models become computationally dense and slow down the entire execution pipeline. The delay between raw data input and actionable market output widens at the exact moment speed holds the highest value. Asset managers recognize that standard computing hardware physically limits the application of standard artificial intelligence during extreme volatility.

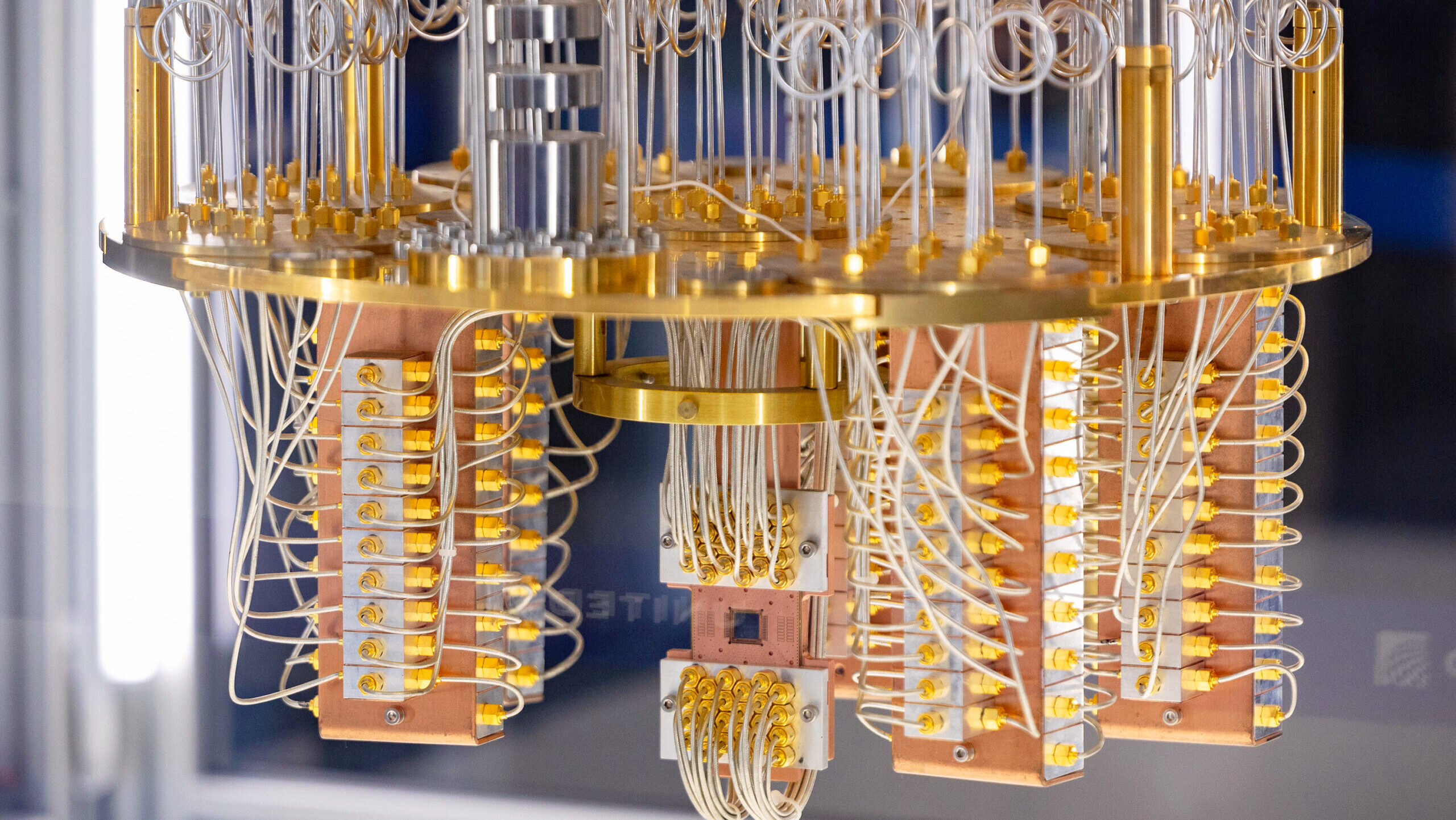

Enter Quantum Mechanics: Redefining Calculation Speed

Quantum computing introduces a completely distinct physical principle to financial data processing. Instead of utilizing binary logic gates, these advanced systems use qubits. A qubit exists in an active state of superposition. It can physically represent a zero, a one, or any combination of both states simultaneously. This unique property allows a quantum processor to calculate multiple outcomes at the exact same time rather than functioning sequentially.

Applying this operational parallel processing to finance shifts the entire math of probability. Consider the analogy of an analyst trying to solve a complex maze. A standard binary computer walks every individual path one by one until it finds the exit. A quantum processing system evaluates the entire labyrinth concurrently and identifies the correct path immediately. The computational advantage scales upwards exponentially as you add more variables to the financial equation.

Executing Complex Risk Assessments

The most immediate application of this concurrent processing capability involves the Monte Carlo simulation. Financial institutions frequently use these heavy simulations to stress-test their portfolios against random market shocks. A thorough Monte Carlo simulation requires calculating millions of randomized price paths for every held asset. On standard hardware, running a high-resolution simulation across a global bank’s entire asset portfolio takes overnight processing in a data center.

Quantum-inspired algorithms focus on reducing that processing time from overnight batches to a few minutes. The ability to understand deep portfolio risk in near real-time changes how investment committees approach capital allocation. A management team can adjust their market exposure before a minor equity correction becomes a structural portfolio failure. The speed of calculation directly preserves capital.

The Mechanics of Portfolio Optimization

Modern Portfolio Theory revolves around finding the exact mathematical mix of assets to maximize expected returns for a specifically predefined level of risk. Finding that perfect numeric balance is notoriously difficult for standard processors. Locating the single most efficient combination of fifty stocks out of a total universe of five thousand market options is mathematically staggering. System engineers call this specific challenge a combinatorial explosion.

The number of possible asset combinations rapidly exceeds the number of atoms in the visible universe. Standard desktop computers and server clusters rely on approximation algorithms to find a mathematically acceptable answer. Finding the absolute best theoretical combination would take standard processors centuries to compute. Quantum computing actively specializes in solving these exact types of heavy optimization problems.

The underlying quantum hardware naturally gravitates toward the lowest energy state. In algorithm design, this physical decay translates perfectly to finding the optimal mathematical solution of a complex function. By mapping financial assets to individual qubits, system engineers can theoretically identify the absolute most efficient portfolio distribution available at any given second. The implications for index fund rebalancing, pension capital allocations, and individual wealth management are massive.

Practical Applications for Crypto and Equities

The theoretical physics behind these processors translates directly into daily market mechanics. Cryptocurrency markets operate twenty-four hours a day across decentralized global exchanges. This continuous global trading volume generates an unprecedented stream of disjointed pricing data across disparate liquidity pools. Manual trading cannot track hundreds of order books concurrently. Standard algorithms attempt to identify arbitrage opportunities across these fragmented exchanges but frequently suffer from execution delays. The processing delay often means a price discrepancy vanishes completely before a standard order ever executes.

Quantum-assisted models process the entire order book depth from fifty different exchanges concurrently. This operational speed allows systems to capture fractional price differences that only exist for a few milliseconds. Equities present a distinctly different data challenge. Traditional stock exchanges maintain rigid opening and closing hours. Corporate announcements frequently break over the weekend. Major earnings reports routinely drop immediately after the closing bell sounds. The opening minutes of the New York Stock Exchange undergo extreme volatility as human traders and algorithms attempt to process hours of pent-up news data.

Advanced computational models analyze all the weekend news sentiment and off-hours trading data simultaneously. The integrated systems calculate the optimal mathematical entry price well before the opening bell even rings, positioning the portfolio to absorb the initial volatility spike profitably.

Mitigating Human Emotion Under Pressure

Technical capabilities aside, algorithmic execution completely removes the psychological strain associated with active asset management. Human traders inevitably suffer from behavioral flaws like recency bias and loss aversion. They hold losing positions too long hoping for an unlikely rebound and frequently sell winning positions prematurely just to secure a small profit. A math-based algorithmic system operates strictly on predefined risk parameters. If the mathematical model indicates a necessary sell condition, the system executes the market order without any hesitation.

The Role of Accessible Automated Tools

Institutional trading desks originally monopolized all quantitative analysis. The required server hardware and specialized engineering talent restricted access to the largest global banks and private hedge funds. The broader expansion of cloud computing and direct application programming interfaces has gradually democratized these technical capabilities. A professional managing their own private capital no longer needs to build a local server farm or write complex neural network code from scratch.

Software platforms currently act as secure intermediaries between complex algorithmic processing and the retail user base. They handle the mathematical complexity entirely in the background while providing clean user interfaces. A busy professional examining their available market options might utilize Quantum AI to access automated trading logic. These platforms parse the heavy computational workloads on remote institutional-grade servers.

The individual user simply defines their acceptable risk tolerance levels and broad asset class preferences. The underlying algorithms handle all the active market scanning, statistical pattern recognition, and final trade execution. Software technology serves as a reliable bridge, permitting individuals to apply high-speed crypto and equity tracking strategies that were completely unavailable a decade ago.

A Professional Walkthrough: Implementing Algorithmic Strategies

Incorporating automated systems into your wealth management strategy requires a highly deliberate and calculated approach. Algorithmic technology operates at microsecond speeds. It executes both mathematically profitable logic and poorly designed logic at the exact same pace. A careless software setup actively multiplies financial exposure. Professionals follow a strict implementation sequence to transition from manual analysis to automated systems safely.

First, define the exact operational scope of the automation layer. Decide whether you want the software system to simply generate alerts for your manual review or execute the actual trades autonomously. Cautious professionals always begin with alert-only functionality before trusting any external software with capital.

Second, allocate a strictly segmented capital pool. Connecting an untested algorithmic system to a primary retirement account introduces unacceptable operational risk. Isolate a specific small percentage of your risk capital for early automated testing. The system must prove its mathematical validity in a live environment over several months.

Third, demand rigorous backtesting metrics. Apply the chosen algorithm against dense historical market data covering the past five years. Watch how the software logic performs during high-volatility events like a flash crash or an unexpected global interest rate hike. An algorithm that only functions perfectly in a rising equity market is fundamentally flawed.

Fourth, establish hardware and software redundancy protocols. If your algorithm runs on a local desktop computer, a simple regional power outage interrupts your entire trading logic. Utilizing cloud-hosted financial platforms mitigates most local hardware failures. Restrict all application programming interface access strictly to trading execution. Never grant external software systems the permission to withdraw or transfer capital between accounts.

Security and Infrastructure Considerations

The introduction of exponentially faster computing power creates a distinctly serious friction point in modern cybersecurity. The entire global financial sector relies heavily on standard encryption protocols to protect data and secure money transfers. These classical encryption protocols actively assume that factoring very large prime numbers would take a standard binary computer thousands of years to complete.

A fully mature quantum computer could theoretically solve these exact encryption equations in a matter of days. This predictive capability actively threatens the foundational security of decentralized blockchain networks and centralized banking databases equally. The technology industry has already initiated a transition toward new post-quantum cryptography standards. Cryptographers are currently developing lattice-based mathematical problems designed to resist both classical and advanced quantum decryption attempts.

Institutional trading platforms are systematically upgrading their internal infrastructure to support these new cryptographic security standards. When evaluating any automated market platform, professionals must carefully review the published data handling procedures. Secure processing demands end-to-end encryption for all database storage and very strictly defined permission sets for all automated activity.